In this third blog of the 4 part “

Building The Case” series, I will focus on internal audit solutions – hence specifically

SAP Audit Management, but the series addresses all the SAP solutions supporting the 3 Lines Model: internal control and compliance with SAP Process Control; enterprise risk management with SAP Risk Management; but also fraud detection and investigation with SAP Business Integrity Screening, with a last blog in this series coming up very soon.

SAP Audit Management helps companies review how to streamline internal audits and improve quality by simplifying documentation of evidence, organizing work papers, and creating reports – on-site and remote.

With the

SAP Audit Management Value Calculator you can quantify the benefits of enhancing audits with trusted insights, but also streamlining internal audits and improving their quality with mobile capabilities.

Should you want to get real, useful estimates and data to help you make the case for an internal audit solution, then the

SAP Audit Management Value Calculator should help. Just click on GET STARTED to launch the process!

Before we start, I just want to highlight the fact that this value calculator provides estimated data for illustration purposes only. Actual results or costs may of course vary and may be affected by additional factors that would need to be taken into account when using this information in your business case.

Section 1 – Configure

Value calculations are based on the assumption that today’s total audit costs are equal to the value delivered. But automation will result in efficiencies and increased effectiveness that will increase that value and these are precisely the insights that this value calculator will provide.

In this first step, you’ll be asked to provide your best estimate for various company attributes. Don’t worry, you can then change them to create different scenarios if you wish.

What indicators are required:

- Completed audit engagements in the last 12 months

- Full-time equivalent (FTE) audit resources

- Average annual fully loaded cost per auditor

- Average percentage of time auditors spend on issues, per engagement

- Total annual travel costs for the entire audit team

- Average cost per issue, including documentation and remediation

Section 2 – Manage

A risk-based audit plan will add value by prioritizing audit activities, hence helping the team focus its resources on the audits that matter, when they matter.

With a sound risk-based plan you can:

- Prioritize audit activities to align with the needs of the enterprise

- Communicate plans and resource requirements

- Deploy appropriate resources to the right places

- Easily report plan performance to senior management and the board

What indicators are required:

- Reduction in time spent per issue thanks to risk-based planning

- Average number of issues per audit engagement, regardless of their criticality

Section 3 – Plan

Developing and documenting a plan for each engagement ensures that the audit team has the right skills and knowledge and that the objectives are clear. Good planning increases auditor productivity and reduces audit costs. More findings and lower costs combined together bring value to the entire organization.

With such an approach, the audit team can:

- Establish engagement objectives and scope

- Assess relevant risks

- Plan appropriate and sufficient resources

- Develop and document engagement work programs.

What indicators are required:

- Percentage increase in staff utilization

- Reduction in travel costs in percentage

Section 4 – Perform

Streamlining and automating fieldwork drives efficiency. And of course, being able to lower costs adds direct financial value by reducing audit spend.

This section will focus on the benefits the audit team can get:

- Automating the analysis and evaluation

- Streamlining the documentation

- Remotely monitor and supervise the engagement in real time

What indicators are required:

- Average percentage reduction in documentation time spent per audit

- Percentage reduction in testing time, per audit engagement

Section 5 – Communicate

Aggregating and communicating audit results in a manual environment can be time consuming and prone to errors and omissions. This section will focus on benefits that the audit team can generate by:

- Improving communication on engagement objectives, scope, conclusions, findings, and recommendations

- Determining communication criteria

- Disseminating results efficiently and effectively

What indicators are required:

- Percentage reduction in time spent on issue tracking and follow

- Reduction in time spent preparing and distributing reports, in percentage

Section 6 – Monitor

Finally, audit recommendations only add value if they are communicated and addressed. Streamlining the reporting and issue tracking process leads to quicker resolution and action.

This last section before getting the results will focus on benefits that audit can achieve by:

- Monitoring the disposition of results reported to management

- Establishing a follow up process to monitor management actions

- Faster capturing of incidents and losses

- Monitoring the disposition of consulting engagements

What indicators are required:

- Percentage reduction in time spent on analyzing, aggregating, and issuing high-level thematic reports to the board and senior executives

- Percentage reduction in repeat audit findings

- Percentage of time saved in resolving issues

Section 7 – Total Value

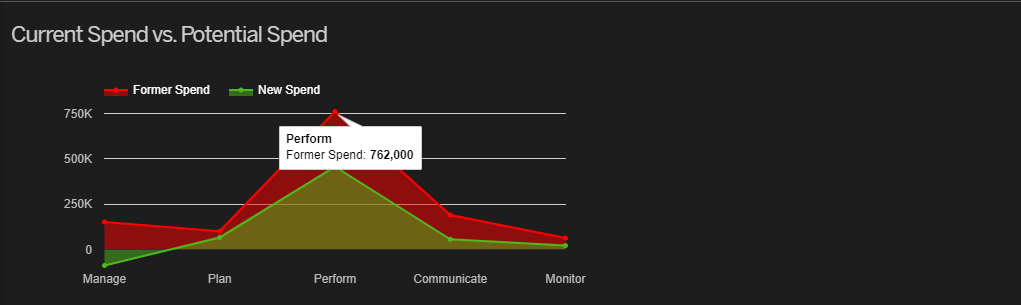

That’s it! This last section is a summary that displays the potential value gain achievable with SAP Audit Management. It includes 4 graphs:

Current Spend vs. Potential Spend

Difference in Spend (lighter color is previous state and darker colors represents potential shift)

Total Gains by Control Step

Total Spend and Gain

Registration is not required, and you can change your assumptions as many times as you wish. So why not give it a try?

What about you, what other variables do you take into consideration when building the case for an audit management solution? I look forward to reading your thoughts and comments either on this blog or on Twitter

@TFrenehard

And stay tuned on the

GRCTuesdays site for the other blogs on internal control, risk management and fraud detection and investigation.