- SAP Community

- Products and Technology

- Technology

- Technology Blogs by SAP

- Global convergence through IFRS - Part II

Technology Blogs by SAP

Learn how to extend and personalize SAP applications. Follow the SAP technology blog for insights into SAP BTP, ABAP, SAP Analytics Cloud, SAP HANA, and more.

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Former Member

Options

- Subscribe to RSS Feed

- Mark as New

- Mark as Read

- Bookmark

- Subscribe

- Printer Friendly Page

- Report Inappropriate Content

11-25-2008

4:48 AM

Continuing on the blog series for IFRS, in this blog we discuss the things in bold below

- History of IFRS and why/how it came into existence

- Basic principles of IFRS

- IFRS roadmap by different countries

- List of IFRS

- IFRS deep dive on standards

- Significant differences between IFRS and country GAAP e.g. US GAAP

- How IFRS is enabled in SAP products

- How should your company plan for IFRS adoption

- What global opportunities exists for IFRS consultants…..and more

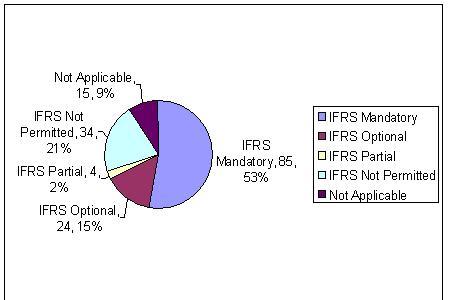

Many countries have adapted IFRS across the globe. They have clearly indicated a roadmap whereby companies in their respective countries have to adapt IFRS. The below graphic represents a rough spread in terms of which countries have adopted, are moving towards adoption

"

" Information, updated as on August 2008, for 162 countries (or jurisdictions):

- IFRSs required for all — 85 countries

- IFRSs permitted — 24 countries

- IFRSs required for some — 4 countries

- IFRSs not permitted — 34 countries

- No stock exchange — 15 countries

So you can note that about 113 countries have signed up mandatorily or optionally for IFRS.

Let us examine some of the countries perspective.

EU countries were the first to adapt IFRS and there was a mandate to get all of the listed companies to follow IFRS by 2005.

US has taken significant steps to move towards IFRS. In late August 2008, the U.S. Securities and Exchange Commission (SEC) announced its proposal on the roadmap that could lead to requiring public companies to issue their financial statements under IFRS in 2014. However the final determination of the adoption would be made by 2011. For this SEC has identified few milestones that would enable it to take a decision on transition of US GAAP to IFRS

- Continued improvement in IFRS — in line with the objective of continuous improvement as part of the convergence between U.S. GAAP and IFRS.

- Change in the IASB organization — to reinforce its accountability and to stabilize its funding. Earlier this year, the Trustees of IASB proposed to set up an oversight committee, which would include the SEC, the European Commission and the U.K.’s Financial Services Authority.

- Develop an IFRS eXtensible Business Reporting Language (XBRL) taxonomy — mirroring the existing U.S. GAAP XBRL taxonomy. The International Accounting Standards Committee (IASC) Foundation announced the publication of the IFRS taxonomy guide on August 28, 2008.

- Training and education — of users, such as preparers, auditors or investors in the U.S.

Large companies that meet the following criteria would qualify for this early adoption:

- The company must be in the top-20 of its industry;

- IFRS must be the most used accounting standard in the industry, which does not mean that more than 50 percent of companies are under IFRS; and

- The company must receive a no objection letter from the SEC.

While the SEC has singled out about 110 companies that would meet this criterion, it expects to exclude large companies with activities in which U.S. groups are dominant from early adoption.

While the SEC has made no set decision, both companies and CPAs should be prepared for what’s to come. The roadmap presents a clear path to the transition to IFRS, but the SEC has decided to stay short on the decision, which has been postponed until 2011, and to leave open the discussion.

However, a company’s strategy to wait until 2011 for the SEC decision on the transition towards IFRS may backfire since once the decision is made, there would be almost no time to move properly to IFRS.

Experience shows that the transition to IFRS will impact not only company’s accounting department, but the entire company because:

- Business decisions will be impacted by the accounting standards. For example, 1) in general, while research and development costs are expensed under U.S. GAAP, they can be capitalized under IFRS; and 2) hedge accounting is different under both standards and will require a change in processes in order to maintain a similar result;

- Tax planning has to be revalued; and

- Internal control and processes have to be reviewed.

· The reporting, including budgeting, will have to be revisited along with systems in order to maintain an effective management of the performance.

China decided that Chinese companies would adopt IFRS in 2006. This move was taken to boost foreign investment into china. However state run enterprises would be execmpted from the ‘related-party’ disclosures.

Japan agreed to move to IFRS by 2011. Japan’s claim was that its existing GAAP was similar to IFRS and saw no issue in Japenese companies moving to IFRS in that timeframe.

South Korea indicated that it will adopt IFRS by 2011. India has also indicated it would adopt IFRS by 2011.

As seen above many of the leading developing countries have either adopted or specified a clear roadmap for adoption of IFRS. This presents a huge opportunity for the world to become unified in terms of financial governance and reporting.

4. List of IFRSIFRS is a combination of IFRS and IAS standards and is very exhaustive. The below list provides what each one is and what they cover:

IFRS 1 – First time adoption of IFRS

IFRS 5 – Non current assets held for sale and discontinued operations

IFRS 6 – Exploration for and evaluation of mineral assets

IFRS 7 – Financial Instruments : disclosures

IFRS also includes the International Accounting Standards that specify accounting guidelines to be followed in different areas. There are about 41 International Accounting Standards

IAS 1 – Presentation of Financial Statements

IAS 8 – Accounting Policies, Changes in Accounting Estimates and Errors

IAS 10 – Events after balance sheet date

IAS 11 – Construction contracts

IAS 14 – Segment ReportingIAS 16 – Property, Plant and Equipment

IAS 20 – Accounting for Government Grants and Disclosure of Government Assistance

IAS 21 – Effects of Changes in Foreign Exchange Rates

IAS 24 – Related Party Disclosures

IAS 26 – Accounting and Reporting by Retirement Benefit Plans

IAS 27 – Consolidated and Separate Financial Statements

IAS 28 – Investments in Associates

IAS 29 – Financial Reporting in Hyperinflationary Economies

IAS 31 – Interests in Joint Ventures

IAS 34 – Interim Financial Reporting

IAS 37 – Provisions, Contingent Liabilities and Contingent Assets

IAS 39 – Financial Instruments: Recognition and Movement

You can see that some missing numbers in the above list , these are standards that have been combined into others or removed, and therefore they no longer exist.

Understanding the above standards in detail would be valuable for Business Process Expert consultants who want to implement IFRS.

We would continue further on this blog series as we move into more technical aspects of IFRS and logically move towards how SAP’s solutions are suited to enable IFRS.

Also refer Global convergence through IFRS - Part I of the blog series.

- SAP Managed Tags:

- BW (SAP Business Warehouse)

3 Comments

You must be a registered user to add a comment. If you've already registered, sign in. Otherwise, register and sign in.

Labels in this area

-

ABAP CDS Views - CDC (Change Data Capture)

2 -

AI

1 -

Analyze Workload Data

1 -

BTP

1 -

Business and IT Integration

2 -

Business application stu

1 -

Business Technology Platform

1 -

Business Trends

1,658 -

Business Trends

111 -

CAP

1 -

cf

1 -

Cloud Foundry

1 -

Confluent

1 -

Customer COE Basics and Fundamentals

1 -

Customer COE Latest and Greatest

3 -

Customer Data Browser app

1 -

Data Analysis Tool

1 -

data migration

1 -

data transfer

1 -

Datasphere

2 -

Event Information

1,400 -

Event Information

74 -

Expert

1 -

Expert Insights

177 -

Expert Insights

348 -

General

1 -

Google cloud

1 -

Google Next'24

1 -

GraphQL

1 -

Kafka

1 -

Life at SAP

780 -

Life at SAP

14 -

Migrate your Data App

1 -

MTA

1 -

Network Performance Analysis

1 -

NodeJS

1 -

PDF

1 -

POC

1 -

Product Updates

4,575 -

Product Updates

391 -

Replication Flow

1 -

REST API

1 -

RisewithSAP

1 -

SAP BTP

1 -

SAP BTP Cloud Foundry

1 -

SAP Cloud ALM

1 -

SAP Cloud Application Programming Model

1 -

SAP Datasphere

2 -

SAP S4HANA Cloud

1 -

SAP S4HANA Migration Cockpit

1 -

Technology Updates

6,871 -

Technology Updates

483 -

Workload Fluctuations

1

Related Content

- First steps to work with SAP Cloud ALM Deployment scenario for SAP ABAP systems (7.40 or higher) in Technology Blogs by SAP

- S_ALR_87013611 Report Painter report to Internal Table in Technology Q&A

- Inside SAP: Discover How SAP’s IT Drives Transformation and Innovation in Technology Blogs by SAP

- Establishing Trust with Custom Identity Provider for Platform Users failed in Technology Q&A

- Exploring ML Explainability in SAP HANA PAL – Classification and Regression in Technology Blogs by SAP

Top kudoed authors

| User | Count |

|---|---|

| 15 | |

| 11 | |

| 10 | |

| 9 | |

| 8 | |

| 8 | |

| 7 | |

| 7 | |

| 7 | |

| 7 |