- SAP Community

- Products and Technology

- Enterprise Resource Planning

- ERP Blogs by Members

- S/4HANA in 5 minutes or less - Interaction between...

Enterprise Resource Planning Blogs by Members

Gain new perspectives and knowledge about enterprise resource planning in blog posts from community members. Share your own comments and ERP insights today!

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Private_Member_

Explorer

Options

- Subscribe to RSS Feed

- Mark as New

- Mark as Read

- Bookmark

- Subscribe

- Printer Friendly Page

- Report Inappropriate Content

09-11-2020

1:59 PM

During the last S/4HANA conversions, which I was fortunate enough to accompany, it became particularly apparent that, in addition to the technological challenges and the adaptation of new functions, the cooperation between departments had to be adapted, sometimes drastically.

One of the most popular challenges was the need to bring internal accounting (CO) and financial accounting (FI) closer together. Here, the responsibilities were reassigned with every S/4HANA transformation I know of.

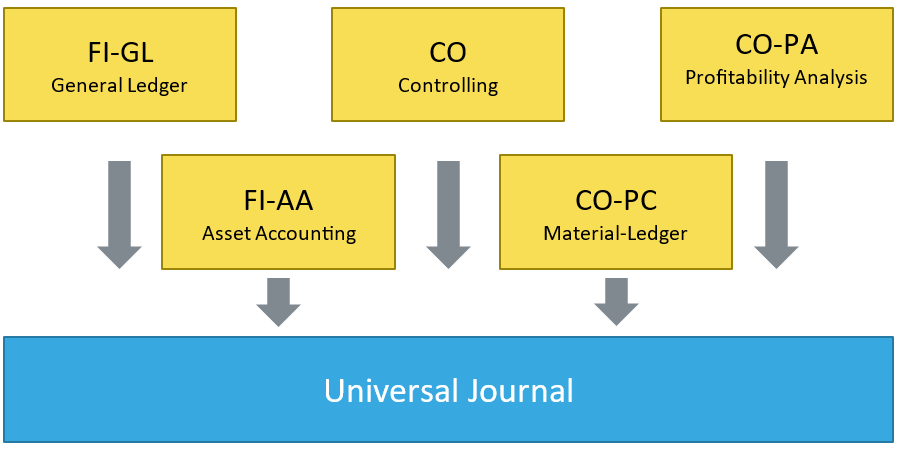

The introduction of the so-called "Universal Journal" in S/4HANA Finance is probably the innovation that affects every customer, regardless of industry. SAP is pursuing three objectives with the complete transfer of the previous distributed data model into a central data model.

The previous division between the Controlling (CO) and Financial Accounting (FI) modules reflected the strict division of the two accounting areas that has been customary in Germany for fifty years. In the processes and data management of the SAP ERP system, this separation was achieved by transferring costs, after they had been entered in accounts in financial accounting, to separate objects in the controlling sphere - the so-called primary cost elements - when the appropriate customizing was carried out. These cost elements have the same number as the corresponding FI account, but are otherwise completely independent of the FI area. All repostings, distributions and activity accounting in Controlling are then carried out in separate data sets, separate from the financial accounting. If account assignments from the FI area were influenced by controlling processes, a considerable reconciliation effort was necessary at the end of the period.

By merging the internal and external accounting groups in the Universal Journal, these reconciliations are no longer necessary. This naturally leads to a merging of the areas of responsibility. The most obvious change is the integration of controlling into the account logic of financial accounting. This means that the secondary cost elements, previously objects which were only known in the Controlling data model for redistribution, settlements and calculations, will now have their own account, just as the primary cost elements already have. Since the rule already applied in the ERP system for primary cost elements was that the cost element number had to correspond exactly to the corresponding FI G/L account number, while for secondary cost element numbers it was generally not allowed to have a G/L account with the same number, the automatic creation of secondary cost elements as accounts during the S/4HANA conversion never leads to errors. Nevertheless, these new accounts under S/4HANA now appear in FI balance lists, balance sheets (unassigned accounts) and similar reports if they are not explicitly excluded in the filter. In addition, in addition to employees from financial accounting, controlling employees also work with the transactions for creating G/L accounts (e.g. FS00).

For this purpose you have to make sure to plan appropriate training courses, adjustments of the process flows and authorization changes in the project.

In the interaction between financial accounting and Controlling, it is also the period-end closing, which always requires special attention during the conversion to S/4HANA. Since the data basis for both groups is now the Universal Journal, closing the posting period in SAP FI, you automatically won't be able to make any postings from controlling applications. This also applies if it is only a transfer posting between a CO account assignment object such as a cost center or internal order without changing the balance on the corresponding G/L account. The possibility to carry out FI-relevant postings from CO applications even after the closing date of the financial accounting can be created via new setting options. Nevertheless, a closer coordination between the departments under S/4HANA is advisable.

The introduction of the Universal Journal promotes the growing together of the two accounting systems. In projects, it repeatedly turned out to me that the two topics of "month-end closing and period locking" and the joint creation of master data (accounts) require early and open discussion between the traditional external and internal accounting departments. The technical possibilities are all available. Now it requires unbiased minds on both sides to define the appropriate accounting process which unleash the power of S/4HANA.

One of the most popular challenges was the need to bring internal accounting (CO) and financial accounting (FI) closer together. Here, the responsibilities were reassigned with every S/4HANA transformation I know of.

SAP CO and FI - nearly all customers are affected

The introduction of the so-called "Universal Journal" in S/4HANA Finance is probably the innovation that affects every customer, regardless of industry. SAP is pursuing three objectives with the complete transfer of the previous distributed data model into a central data model.

- To create a single, redundancy-free point of truth for internal and external accounting, including its sub-modules This will also allow puncture possibilities down to the level of single items.

- Real-time integration of all internal and external accounting postings and thus the elimination of the reconciliation processes previously required at the end of the period.

- Utilisation of the technical possibilities of the HANA database platform by resolving various individual, summary and index tables and transferring them to a central line item table.

The Universal Journal contains not only SAP FI data but also CO

Separation of data led to a separation of responsibilities

The previous division between the Controlling (CO) and Financial Accounting (FI) modules reflected the strict division of the two accounting areas that has been customary in Germany for fifty years. In the processes and data management of the SAP ERP system, this separation was achieved by transferring costs, after they had been entered in accounts in financial accounting, to separate objects in the controlling sphere - the so-called primary cost elements - when the appropriate customizing was carried out. These cost elements have the same number as the corresponding FI account, but are otherwise completely independent of the FI area. All repostings, distributions and activity accounting in Controlling are then carried out in separate data sets, separate from the financial accounting. If account assignments from the FI area were influenced by controlling processes, a considerable reconciliation effort was necessary at the end of the period.

A tear down of the known walls between the departments is needed

By merging the internal and external accounting groups in the Universal Journal, these reconciliations are no longer necessary. This naturally leads to a merging of the areas of responsibility. The most obvious change is the integration of controlling into the account logic of financial accounting. This means that the secondary cost elements, previously objects which were only known in the Controlling data model for redistribution, settlements and calculations, will now have their own account, just as the primary cost elements already have. Since the rule already applied in the ERP system for primary cost elements was that the cost element number had to correspond exactly to the corresponding FI G/L account number, while for secondary cost element numbers it was generally not allowed to have a G/L account with the same number, the automatic creation of secondary cost elements as accounts during the S/4HANA conversion never leads to errors. Nevertheless, these new accounts under S/4HANA now appear in FI balance lists, balance sheets (unassigned accounts) and similar reports if they are not explicitly excluded in the filter. In addition, in addition to employees from financial accounting, controlling employees also work with the transactions for creating G/L accounts (e.g. FS00).

For this purpose you have to make sure to plan appropriate training courses, adjustments of the process flows and authorization changes in the project.

The account sheet is the only source for master data for FI and CO in S/4HANA

In the interaction between financial accounting and Controlling, it is also the period-end closing, which always requires special attention during the conversion to S/4HANA. Since the data basis for both groups is now the Universal Journal, closing the posting period in SAP FI, you automatically won't be able to make any postings from controlling applications. This also applies if it is only a transfer posting between a CO account assignment object such as a cost center or internal order without changing the balance on the corresponding G/L account. The possibility to carry out FI-relevant postings from CO applications even after the closing date of the financial accounting can be created via new setting options. Nevertheless, a closer coordination between the departments under S/4HANA is advisable.

Conclusion

The introduction of the Universal Journal promotes the growing together of the two accounting systems. In projects, it repeatedly turned out to me that the two topics of "month-end closing and period locking" and the joint creation of master data (accounts) require early and open discussion between the traditional external and internal accounting departments. The technical possibilities are all available. Now it requires unbiased minds on both sides to define the appropriate accounting process which unleash the power of S/4HANA.

- SAP Managed Tags:

- SAP S/4HANA,

- SAP S/4HANA Finance,

- FIN Controlling,

- FIN General Ledger

1 Comment

You must be a registered user to add a comment. If you've already registered, sign in. Otherwise, register and sign in.

Labels in this area

-

"mm02"

1 -

A_PurchaseOrderItem additional fields

1 -

ABAP

1 -

ABAP Extensibility

1 -

ACCOSTRATE

1 -

ACDOCP

1 -

Adding your country in SPRO - Project Administration

1 -

Advance Return Management

1 -

AI and RPA in SAP Upgrades

1 -

Approval Workflows

1 -

ARM

1 -

ASN

1 -

Asset Management

1 -

Associations in CDS Views

1 -

auditlog

1 -

Authorization

1 -

Availability date

1 -

Azure Center for SAP Solutions

1 -

AzureSentinel

2 -

Bank

1 -

BAPI_SALESORDER_CREATEFROMDAT2

1 -

BRF+

1 -

BRFPLUS

1 -

Bundled Cloud Services

1 -

business participation

1 -

Business Processes

1 -

CAPM

1 -

Carbon

1 -

Cental Finance

1 -

CFIN

1 -

CFIN Document Splitting

1 -

Cloud ALM

1 -

Cloud Integration

1 -

condition contract management

1 -

Connection - The default connection string cannot be used.

1 -

Custom Table Creation

1 -

Customer Screen in Production Order

1 -

Data Quality Management

1 -

Date required

1 -

Decisions

1 -

desafios4hana

1 -

Developing with SAP Integration Suite

1 -

Direct Outbound Delivery

1 -

DMOVE2S4

1 -

EAM

1 -

EDI

2 -

EDI 850

1 -

EDI 856

1 -

EHS Product Structure

1 -

Emergency Access Management

1 -

Energy

1 -

EPC

1 -

Find

1 -

FINSSKF

1 -

Fiori

1 -

Flexible Workflow

1 -

Gas

1 -

Gen AI enabled SAP Upgrades

1 -

General

1 -

generate_xlsx_file

1 -

Getting Started

1 -

HomogeneousDMO

1 -

IDOC

2 -

integration

1 -

Learning Content

2 -

LogicApps

2 -

low touchproject

1 -

Maintenance

1 -

management

1 -

Material creation

1 -

Material Management

1 -

MD04

1 -

MD61

1 -

methodology

1 -

Microsoft

2 -

MicrosoftSentinel

2 -

Migration

1 -

MRP

1 -

MS Teams

2 -

MT940

1 -

Newcomer

1 -

Notifications

1 -

Oil

1 -

open connectors

1 -

Order Change Log

1 -

ORDERS

2 -

OSS Note 390635

1 -

outbound delivery

1 -

outsourcing

1 -

PCE

1 -

Permit to Work

1 -

PIR Consumption Mode

1 -

PIR's

1 -

PIRs

1 -

PIRs Consumption

1 -

PIRs Reduction

1 -

Plan Independent Requirement

1 -

Premium Plus

1 -

pricing

1 -

Primavera P6

1 -

Process Excellence

1 -

Process Management

1 -

Process Order Change Log

1 -

Process purchase requisitions

1 -

Product Information

1 -

Production Order Change Log

1 -

Purchase requisition

1 -

Purchasing Lead Time

1 -

Redwood for SAP Job execution Setup

1 -

RISE with SAP

1 -

RisewithSAP

1 -

Rizing

1 -

S4 Cost Center Planning

1 -

S4 HANA

1 -

S4HANA

3 -

Sales and Distribution

1 -

Sales Commission

1 -

sales order

1 -

SAP

2 -

SAP Best Practices

1 -

SAP Build

1 -

SAP Build apps

1 -

SAP Cloud ALM

1 -

SAP Data Quality Management

1 -

SAP Maintenance resource scheduling

2 -

SAP Note 390635

1 -

SAP S4HANA

2 -

SAP S4HANA Cloud private edition

1 -

SAP Upgrade Automation

1 -

SAP WCM

1 -

SAP Work Clearance Management

1 -

Schedule Agreement

1 -

SDM

1 -

security

2 -

Settlement Management

1 -

soar

2 -

SSIS

1 -

SU01

1 -

SUM2.0SP17

1 -

SUMDMO

1 -

Teams

2 -

User Administration

1 -

User Participation

1 -

Utilities

1 -

va01

1 -

vendor

1 -

vl01n

1 -

vl02n

1 -

WCM

1 -

X12 850

1 -

xlsx_file_abap

1 -

YTD|MTD|QTD in CDs views using Date Function

1

- « Previous

- Next »

Related Content

- Time Constraints - Purchase order wprkflow approval in Enterprise Resource Planning Q&A

- Check if PDF is interactive in Enterprise Resource Planning Q&A

- How do you retrieve an PM equipment using a linked FI asset number? (ABAP) in Enterprise Resource Planning Q&A

- SAP Background Job Processing in Enterprise Resource Planning Blogs by Members

- How to Set Up Approval Workflows for Supplier Down Payment Requests in Enterprise Resource Planning Blogs by SAP

Top kudoed authors

| User | Count |

|---|---|

| 2 | |

| 2 | |

| 2 | |

| 2 | |

| 1 | |

| 1 | |

| 1 | |

| 1 | |

| 1 | |

| 1 |