- SAP Community

- Products and Technology

- Enterprise Resource Planning

- ERP Blogs by Members

- Product Cost By Order Cycle

Enterprise Resource Planning Blogs by Members

Gain new perspectives and knowledge about enterprise resource planning in blog posts from community members. Share your own comments and ERP insights today!

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

former_member49

Participant

Options

- Subscribe to RSS Feed

- Mark as New

- Mark as Read

- Bookmark

- Subscribe

- Printer Friendly Page

- Report Inappropriate Content

11-30-2017

9:17 PM

Product Costing is the one of the core responsibility of the Controlling Department for every manufacturing concern, which varies from business to business depending on nature of its Products and Production. Its supports the organization in making loads of strategic decision along with other functional areas.Gaining some expertise of SAP Product Costing over the past few years, this is my attempt to provide the overview of SAP product costing process.

The Cost Object Controlling is tool provided by SAP CO module to cater Product costing activities in an organization. Under Cost Object Controlling lies the following costing objects,

The figure below illustrate the use of Product Costing objects in pertaining Production environment,

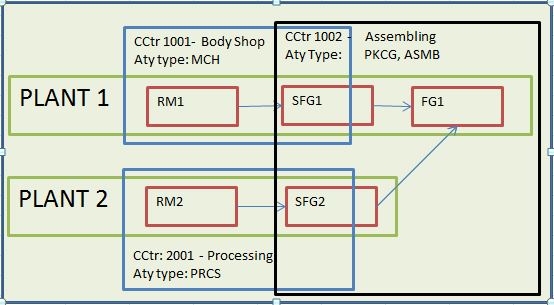

In this blog I have tried to explain the process of Product Cost by Order with typical example of manufacturing Finished Material FG1 on two different Plants 1 & 2, the BOM (Bill of Material) and Routing required to manufactured one unit of FG1 is depicted in the figure below,

Procurement of Raw Material (RM1 for Plant 1 and RM2 for Plant 2),

In the below scenario, we have procure RM1 from two different Vendors at 50:50 ratio. While RM2 is procure from only one Vendor.

Now, we are going to create two Production orders for quantity 150 and 450, the prerequisite for creating Production Order is,

Below is the Production Process cycle,

In our scenario we are using Collective orders With Automatic Goods Movements. i-e; if we create Production order for FERT Material the Production Orders for its semi-Finished good (HALB) gets automatically created.

To Create a collective order, one of the SFGs must have a special procurement key 81 in its MRP/Costing view of master data.

After creating Production Order we perform Good Issue for RMs and SFGs in respective orders, we do this separately through MIGO (movt type: 261) or using MB1A or during confirmation of activities CO11N which is our next step, as shown in figure below.

Info : In case of errors in posting of goods movements , goods movements with errors can reprocessed by,

Alternatively we can cancel confirmation using T-code : CO13 and create again

As in our scenario, we will execute two Production Orders using the below Production process, for quantity 150 & 450.

Now, we post Actual Costs/Expenses incurred on the Production Cost centers 1001, 2001 and 1002 during the month using t-code F-02.

MONTH END ACTIVITIES,

You need to calculate Actual activity Price, by using t-Code KSS2 'Activity Splitting' and KSII 'Actual Activity Price Calculation' or you can enter it manually through t-code KBK6.

Now, you do Revaluation of Activities posted to Production Order at Actual Price by using t-code CON2/ MFN2.

Note: You don't need to perform this step if you have activated Actual costing /Material Ledger and have selected '2' = Update is active and relevant to price determination. As a result of which, Plan/actual variances of cost center are debited to the material instead of charging to Production variance when calculating actual prices of activities during Single –Level Price determination in Actual Costing run.

Below are the screenshots for production cost centers report S_ALR_87013611 for analysis, before and after executing CON2.

Now, we ran the t-code CO43 to calculate overhead based on costing sheet. As a result of this transaction overhead amount calculated is credited to overhead cost center and debited to Production order.

Now, to calculate Work in Progress we run t-code KKAO, as result of this WIP for partially delivered orders (whose status is not TECO or DLV) is calculated but not posted to Finance.

Now, KKS1 is executed to calculate variances for Production order whose statuses are TECO or DLV (delivered). Similar to WIP calculation this transaction only calculates variances as shown in figure below,

After calculating WIP and Variances, now the time comes to record them in Financial Accounting by settling Production order through t-code: CO88/ KO88. As a result of this transaction, along with accounting documents the CO-PA settlement for variance also took place resulting in generation of CO-PA documents with record type C.

The small overview of the customizing setting (spro) for variance settlement to FI and CO-PA are shown in figure below,

The pertaining accounting documents generated are also shown in figure below,

Reports to Analyze production Order,

The boxes with green border line in the above figure shows the reports for Production order. The purpose of them are as follows,

This blog provides mere overview of Product Cost by Order process. In the next blog I will discuss the Product Cost by Period Cycle. Till then readers are requested to keep patience and don't forget to provide feedback for this post.

I appreciate the time you took to read this blog.

The Cost Object Controlling is tool provided by SAP CO module to cater Product costing activities in an organization. Under Cost Object Controlling lies the following costing objects,

- Product Costing By Order

- Product Costing By Product Cost Collector

- Product Costing By Sales order

The figure below illustrate the use of Product Costing objects in pertaining Production environment,

In this blog I have tried to explain the process of Product Cost by Order with typical example of manufacturing Finished Material FG1 on two different Plants 1 & 2, the BOM (Bill of Material) and Routing required to manufactured one unit of FG1 is depicted in the figure below,

Procurement of Raw Material (RM1 for Plant 1 and RM2 for Plant 2),

In the below scenario, we have procure RM1 from two different Vendors at 50:50 ratio. While RM2 is procure from only one Vendor.

Now, we are going to create two Production orders for quantity 150 and 450, the prerequisite for creating Production Order is,

- BOM master for Finished good material should be created through CS01

- Routing for Finished Good Material must be created using t-Code: CR01

- Required quantity of Raw Materials should be procured (as shown above) or available in stock.

Below is the Production Process cycle,

In our scenario we are using Collective orders With Automatic Goods Movements. i-e; if we create Production order for FERT Material the Production Orders for its semi-Finished good (HALB) gets automatically created.

To Create a collective order, one of the SFGs must have a special procurement key 81 in its MRP/Costing view of master data.

After creating Production Order we perform Good Issue for RMs and SFGs in respective orders, we do this separately through MIGO (movt type: 261) or using MB1A or during confirmation of activities CO11N which is our next step, as shown in figure below.

Info : In case of errors in posting of goods movements , goods movements with errors can reprocessed by,

- Reprocessing whole confirmation :- T-code : CO16N

- Reprocessing only Actual costs :- T-code :COFC

- Reprocessing only Goods Movements :- T-code :COGI

Alternatively we can cancel confirmation using T-code : CO13 and create again

As in our scenario, we will execute two Production Orders using the below Production process, for quantity 150 & 450.

Now, we post Actual Costs/Expenses incurred on the Production Cost centers 1001, 2001 and 1002 during the month using t-code F-02.

MONTH END ACTIVITIES,

You need to calculate Actual activity Price, by using t-Code KSS2 'Activity Splitting' and KSII 'Actual Activity Price Calculation' or you can enter it manually through t-code KBK6.

Now, you do Revaluation of Activities posted to Production Order at Actual Price by using t-code CON2/ MFN2.

Note: You don't need to perform this step if you have activated Actual costing /Material Ledger and have selected '2' = Update is active and relevant to price determination. As a result of which, Plan/actual variances of cost center are debited to the material instead of charging to Production variance when calculating actual prices of activities during Single –Level Price determination in Actual Costing run.

Below are the screenshots for production cost centers report S_ALR_87013611 for analysis, before and after executing CON2.

Now, we ran the t-code CO43 to calculate overhead based on costing sheet. As a result of this transaction overhead amount calculated is credited to overhead cost center and debited to Production order.

Now, to calculate Work in Progress we run t-code KKAO, as result of this WIP for partially delivered orders (whose status is not TECO or DLV) is calculated but not posted to Finance.

Now, KKS1 is executed to calculate variances for Production order whose statuses are TECO or DLV (delivered). Similar to WIP calculation this transaction only calculates variances as shown in figure below,

After calculating WIP and Variances, now the time comes to record them in Financial Accounting by settling Production order through t-code: CO88/ KO88. As a result of this transaction, along with accounting documents the CO-PA settlement for variance also took place resulting in generation of CO-PA documents with record type C.

The small overview of the customizing setting (spro) for variance settlement to FI and CO-PA are shown in figure below,

The pertaining accounting documents generated are also shown in figure below,

Reports to Analyze production Order,

The boxes with green border line in the above figure shows the reports for Production order. The purpose of them are as follows,

- T-Code: KE24 - Display Actual Line Items: CO-PA - to analyze the Variances settled to CO-PA.

- T-Code: COMLWIPDISP - Display WIP at Actual Cost. - to analyze the WIP calculated for orders which are not TECO or DLV

- T-Code: KOC4 - Production Order Report - Actual/Plan/Target/ Variance, to analyze costs posted on production orders.

This blog provides mere overview of Product Cost by Order process. In the next blog I will discuss the Product Cost by Period Cycle. Till then readers are requested to keep patience and don't forget to provide feedback for this post.

I appreciate the time you took to read this blog.

- SAP Managed Tags:

- FIN Controlling,

- FIN Cost Object Controlling

2 Comments

You must be a registered user to add a comment. If you've already registered, sign in. Otherwise, register and sign in.

Labels in this area

-

"mm02"

1 -

A_PurchaseOrderItem additional fields

1 -

ABAP

1 -

ABAP Extensibility

1 -

ACCOSTRATE

1 -

ACDOCP

1 -

Adding your country in SPRO - Project Administration

1 -

Advance Return Management

1 -

AI and RPA in SAP Upgrades

1 -

Approval Workflows

1 -

ARM

1 -

ASN

1 -

Asset Management

1 -

Associations in CDS Views

1 -

auditlog

1 -

Authorization

1 -

Availability date

1 -

Azure Center for SAP Solutions

1 -

AzureSentinel

2 -

Bank

1 -

BAPI_SALESORDER_CREATEFROMDAT2

1 -

BRF+

1 -

BRFPLUS

1 -

Bundled Cloud Services

1 -

business participation

1 -

Business Processes

1 -

CAPM

1 -

Carbon

1 -

Cental Finance

1 -

CFIN

1 -

CFIN Document Splitting

1 -

Cloud ALM

1 -

Cloud Integration

1 -

condition contract management

1 -

Connection - The default connection string cannot be used.

1 -

Custom Table Creation

1 -

Customer Screen in Production Order

1 -

Data Quality Management

1 -

Date required

1 -

Decisions

1 -

desafios4hana

1 -

Developing with SAP Integration Suite

1 -

Direct Outbound Delivery

1 -

DMOVE2S4

1 -

EAM

1 -

EDI

2 -

EDI 850

1 -

EDI 856

1 -

EHS Product Structure

1 -

Emergency Access Management

1 -

Energy

1 -

EPC

1 -

Find

1 -

FINSSKF

1 -

Fiori

1 -

Flexible Workflow

1 -

Gas

1 -

Gen AI enabled SAP Upgrades

1 -

General

1 -

generate_xlsx_file

1 -

Getting Started

1 -

HomogeneousDMO

1 -

IDOC

2 -

Integration

1 -

Learning Content

2 -

LogicApps

2 -

low touchproject

1 -

Maintenance

1 -

management

1 -

Material creation

1 -

Material Management

1 -

MD04

1 -

MD61

1 -

methodology

1 -

Microsoft

2 -

MicrosoftSentinel

2 -

Migration

1 -

MRP

1 -

MS Teams

2 -

MT940

1 -

Newcomer

1 -

Notifications

1 -

Oil

1 -

open connectors

1 -

Order Change Log

1 -

ORDERS

2 -

OSS Note 390635

1 -

outbound delivery

1 -

outsourcing

1 -

PCE

1 -

Permit to Work

1 -

PIR Consumption Mode

1 -

PIR's

1 -

PIRs

1 -

PIRs Consumption

1 -

PIRs Reduction

1 -

Plan Independent Requirement

1 -

Premium Plus

1 -

pricing

1 -

Primavera P6

1 -

Process Excellence

1 -

Process Management

1 -

Process Order Change Log

1 -

Process purchase requisitions

1 -

Product Information

1 -

Production Order Change Log

1 -

Purchase requisition

1 -

Purchasing Lead Time

1 -

Redwood for SAP Job execution Setup

1 -

RISE with SAP

1 -

RisewithSAP

1 -

Rizing

1 -

S4 Cost Center Planning

1 -

S4 HANA

1 -

S4HANA

3 -

Sales and Distribution

1 -

Sales Commission

1 -

sales order

1 -

SAP

2 -

SAP Best Practices

1 -

SAP Build

1 -

SAP Build apps

1 -

SAP Cloud ALM

1 -

SAP Data Quality Management

1 -

SAP Maintenance resource scheduling

2 -

SAP Note 390635

1 -

SAP S4HANA

2 -

SAP S4HANA Cloud private edition

1 -

SAP Upgrade Automation

1 -

SAP WCM

1 -

SAP Work Clearance Management

1 -

Schedule Agreement

1 -

SDM

1 -

security

2 -

Settlement Management

1 -

soar

2 -

SSIS

1 -

SU01

1 -

SUM2.0SP17

1 -

SUMDMO

1 -

Teams

2 -

User Administration

1 -

User Participation

1 -

Utilities

1 -

va01

1 -

vendor

1 -

vl01n

1 -

vl02n

1 -

WCM

1 -

X12 850

1 -

xlsx_file_abap

1 -

YTD|MTD|QTD in CDs views using Date Function

1

- « Previous

- Next »

Related Content

- Integration of SAP Service and Asset Manager(SSAM) with SAP FSM to support S/4HANA Service Processes in Enterprise Resource Planning Blogs by SAP

- Kanban with production orders: Scheduling of orders in Enterprise Resource Planning Q&A

- Manage Supply Shortage and Excess Supply with MRP Material Coverage Apps in Enterprise Resource Planning Blogs by SAP

- Sales order line item rejected even though MTO Production order has CNF and DLV status (Strategy 82) in Enterprise Resource Planning Q&A

- Quick Start guide for PLM system integration 3.0 Implementation/Installation in Enterprise Resource Planning Blogs by SAP

Top kudoed authors

| User | Count |

|---|---|

| 2 | |

| 2 | |

| 2 | |

| 2 | |

| 2 | |

| 1 | |

| 1 | |

| 1 | |

| 1 | |

| 1 |