- SAP Community

- Products and Technology

- Enterprise Resource Planning

- ERP Blogs by Members

- Material Ledger + Actual Costing (PUP)

Enterprise Resource Planning Blogs by Members

Gain new perspectives and knowledge about enterprise resource planning in blog posts from community members. Share your own comments and ERP insights today!

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Former Member

Options

- Subscribe to RSS Feed

- Mark as New

- Mark as Read

- Bookmark

- Subscribe

- Printer Friendly Page

- Report Inappropriate Content

01-07-2013

2:45 PM

1. Material Ledger + Actual Costing (PUP)

1.1 - Periodic Unit Price - During the Period

During the period all transactions are valued at standard cost as a preliminary valuation

SAP collects all valuation relevant transaction data in the material ledger for a period

Differences from the preliminary valuation price are posted to price difference accounts

1.2 - Periodic Unit Price - Month end : Single level Price determination

SAP calculates the PUP based on the sum of the price differences, exchange rate differences and production variances in relation to the cumulative inventory quantity and value

Weighted average cost is used to determine PUP

PUP updated in Material Master (statistical)

No variances are rolled to the next production level

1.3 - Periodic Unit Price - Month end : Single level Price determination

Only movements collected in the material Ledger for receipts and other inward/outward movements will effect the PUP

Consumption has no effect on the price

1.4 - Periodic Unit Price - Month end : Multi level Price determination

An actual quantity structure (BOM) is created for all materials within a plant based on goods movements

Variances associated with consumption of lower level materials are rolled up to the higher levels of this actual structure

2. Scenario

2.1 - Receipt and invoicing of raw material

Finished Product FP01 created from single Raw Material RM01.

Price variances on receipt of invoice for RM01.

Production Order utilises half of RM01 stock and incurs lot size variances.

All FP01 sold in period.

RM01 Std @ $10/ton

FP01 Std @ $20/ton

2.2 - Production Order costing and settlement

RM01 Std @ $10/ton

FP01 Std @ $20/ton

2.3 - Sale of finished material

RM01 Std @ $10/ton

FP01 Std @ $20/ton

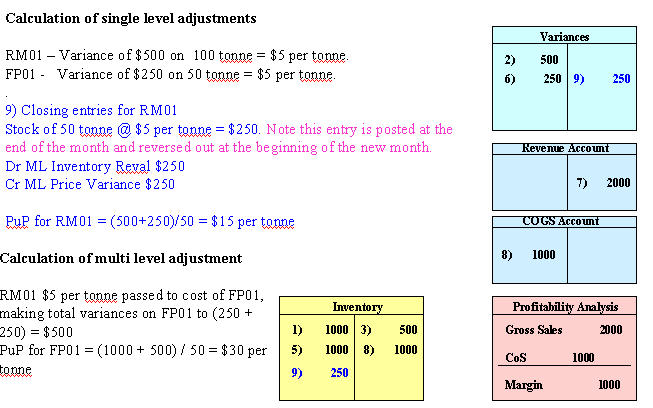

2.4 - PuP calculation and posting

2.5 - Periodic Valuation

RM01 Std @ $10/ton PUP @ $15/ton

FP01 Std @ $20/ton PUP @ $30/ton Sales @ $40/ton

3. Analysis

Standard Price | Moving Average | |

Features |

|

|

| Pros |

|

|

| Cons |

|

|

- SAP Managed Tags:

- FIN (Finance)

9 Comments

You must be a registered user to add a comment. If you've already registered, sign in. Otherwise, register and sign in.

Labels in this area

-

"mm02"

1 -

A_PurchaseOrderItem additional fields

1 -

ABAP

1 -

ABAP Extensibility

1 -

ACCOSTRATE

1 -

ACDOCP

1 -

Adding your country in SPRO - Project Administration

1 -

Advance Return Management

1 -

AI and RPA in SAP Upgrades

1 -

Approval Workflows

1 -

ARM

1 -

ASN

1 -

Asset Management

1 -

Associations in CDS Views

1 -

auditlog

1 -

Authorization

1 -

Availability date

1 -

Azure Center for SAP Solutions

1 -

AzureSentinel

2 -

Bank

1 -

BAPI_SALESORDER_CREATEFROMDAT2

1 -

BRF+

1 -

BRFPLUS

1 -

Bundled Cloud Services

1 -

business participation

1 -

Business Processes

1 -

CAPM

1 -

Carbon

1 -

Cental Finance

1 -

CFIN

1 -

CFIN Document Splitting

1 -

Cloud ALM

1 -

Cloud Integration

1 -

condition contract management

1 -

Connection - The default connection string cannot be used.

1 -

Custom Table Creation

1 -

Customer Screen in Production Order

1 -

Data Quality Management

1 -

Date required

1 -

Decisions

1 -

desafios4hana

1 -

Developing with SAP Integration Suite

1 -

Direct Outbound Delivery

1 -

DMOVE2S4

1 -

EAM

1 -

EDI

2 -

EDI 850

1 -

EDI 856

1 -

edocument

1 -

EHS Product Structure

1 -

Emergency Access Management

1 -

Energy

1 -

EPC

1 -

Financial Operations

1 -

Find

1 -

FINSSKF

1 -

Fiori

1 -

Flexible Workflow

1 -

Gas

1 -

Gen AI enabled SAP Upgrades

1 -

General

1 -

generate_xlsx_file

1 -

Getting Started

1 -

HomogeneousDMO

1 -

IDOC

2 -

Integration

1 -

Learning Content

2 -

LogicApps

2 -

low touchproject

1 -

Maintenance

1 -

management

1 -

Material creation

1 -

Material Management

1 -

MD04

1 -

MD61

1 -

methodology

1 -

Microsoft

2 -

MicrosoftSentinel

2 -

Migration

1 -

MRP

1 -

MS Teams

2 -

MT940

1 -

Newcomer

1 -

Notifications

1 -

Oil

1 -

open connectors

1 -

Order Change Log

1 -

ORDERS

2 -

OSS Note 390635

1 -

outbound delivery

1 -

outsourcing

1 -

PCE

1 -

Permit to Work

1 -

PIR Consumption Mode

1 -

PIR's

1 -

PIRs

1 -

PIRs Consumption

1 -

PIRs Reduction

1 -

Plan Independent Requirement

1 -

Premium Plus

1 -

pricing

1 -

Primavera P6

1 -

Process Excellence

1 -

Process Management

1 -

Process Order Change Log

1 -

Process purchase requisitions

1 -

Product Information

1 -

Production Order Change Log

1 -

Purchase requisition

1 -

Purchasing Lead Time

1 -

Redwood for SAP Job execution Setup

1 -

RISE with SAP

1 -

RisewithSAP

1 -

Rizing

1 -

S4 Cost Center Planning

1 -

S4 HANA

1 -

S4HANA

3 -

Sales and Distribution

1 -

Sales Commission

1 -

sales order

1 -

SAP

2 -

SAP Best Practices

1 -

SAP Build

1 -

SAP Build apps

1 -

SAP Cloud ALM

1 -

SAP Data Quality Management

1 -

SAP Maintenance resource scheduling

2 -

SAP Note 390635

1 -

SAP S4HANA

2 -

SAP S4HANA Cloud private edition

1 -

SAP Upgrade Automation

1 -

SAP WCM

1 -

SAP Work Clearance Management

1 -

Schedule Agreement

1 -

SDM

1 -

security

2 -

Settlement Management

1 -

soar

2 -

SSIS

1 -

SU01

1 -

SUM2.0SP17

1 -

SUMDMO

1 -

Teams

2 -

User Administration

1 -

User Participation

1 -

Utilities

1 -

va01

1 -

vendor

1 -

vl01n

1 -

vl02n

1 -

WCM

1 -

X12 850

1 -

xlsx_file_abap

1 -

YTD|MTD|QTD in CDs views using Date Function

1

- « Previous

- Next »

Related Content

- Advance Return Management complete configuration(SAP ARM) in Enterprise Resource Planning Blogs by Members

- Change material cost in Sales return process during PGR in Enterprise Resource Planning Q&A

- Portfolio Management – Enhanced Financial Planning integration in Enterprise Resource Planning Blogs by SAP

- CK40N costing level doesn't show materials costed without errors in Enterprise Resource Planning Q&A

- How to check the calculation for "Actual Cost Rate Calculation - Cost Centers (KSII)"? in Enterprise Resource Planning Q&A

Top kudoed authors

| User | Count |

|---|---|

| 2 | |

| 2 | |

| 2 | |

| 2 | |

| 2 | |

| 2 | |

| 2 | |

| 1 | |

| 1 | |

| 1 |