![[peanut.jpg]](http://2.bp.blogspot.com/_DhgRhtkULkc/Ss8gspZKXBI/AAAAAAAAABA/NFEpWqAv0C8/s1600/peanut.jpg)

Are your customers profitable? Whenever I ask this question to business executives the immediate response is always "Yes". The comment that typically tends to follow " How can a customer not be profitable? They are purchasing our products and services. They are contributing to our bottom line"

Simply put "Customer Profitability" (CP) is the difference between the revenues earned from and the costs associated with the customer relationship in a specified period. According to the management guru, Philip Kotler, "a profitable customer is a person, household or a company that overtime, yields a revenue stream that exceeds by an acceptable amount the company's cost stream of attracting, selling and servicing the customer".

There is a natural variability of profitability across customers and it is often hard to distinguish the "Profit Creators" from the "Profit Destroyers". In fact, most organizations are likely to have some customers who do not add to the bottom line, but who they are happy to deal with because they add critical mass to the business or because they are a source of knowledge about the needs of a particular customer segment.

The real challenge in measuring customer profitability is identifying the true costs associated with servicing customers and then accurately assigning those costs across customers. The ERP and Performance Management systems that are typically deployed in companies do an excellent job of identifying the revenue and direct costs associated with each customer. However they fall short of answering the fundamental question of "What is the cost of servicing this customer". Most companies tend to apportion the overhead costs, almost like spreading peanut butter. They base it on simple metrics like number of transactions, percentage of total cost of sales etc.

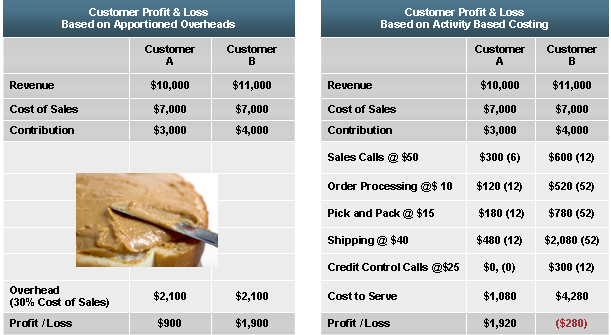

Activity Based Costing can be used to answer these tough questions around costing. It can help identify the right amount of indirect expense to assign to a customer based on the amount of each activity they consume. Let us take a look at a simple example where we analyze customer profitability using the apportionment methodology and Activity Based Costing. We have two customers: A and B. If you review the Customer Profit & Loss based on the two methodologies the results are very different.

When using the apportionment method, the overhead costs are apportioned as a percentage of cost of sales. Based on this it looks like Customer B is the profitable customer. When we look at the same Profit & Loss Statement based on Activity Based Costing the case is totally different. Here we have broken down all the costs associated with servicing the customer. Eg: Sales Calls, Shipping, Packaging etc. In reality, Customer B has a very high “Cost to Serve” and is in fact making a loss. This is fairly typical outcome with apportionment tending to overcost simple customers and undercost those with complex requirements and demands. So without ABC, many organizations are generating totally erroneous reports that can actually lead to managers taking decisions that destroy rather than create value. Not exactly smart - particularly in a downturn. The methodology has been around for 25 years now and it's something that organizations can no longer afford to side step if they want an accurate measurement system for reporting customer profitability.